Introduction: NS&I Raises Premium Bonds Prize Rate to 3.80% for July 2026

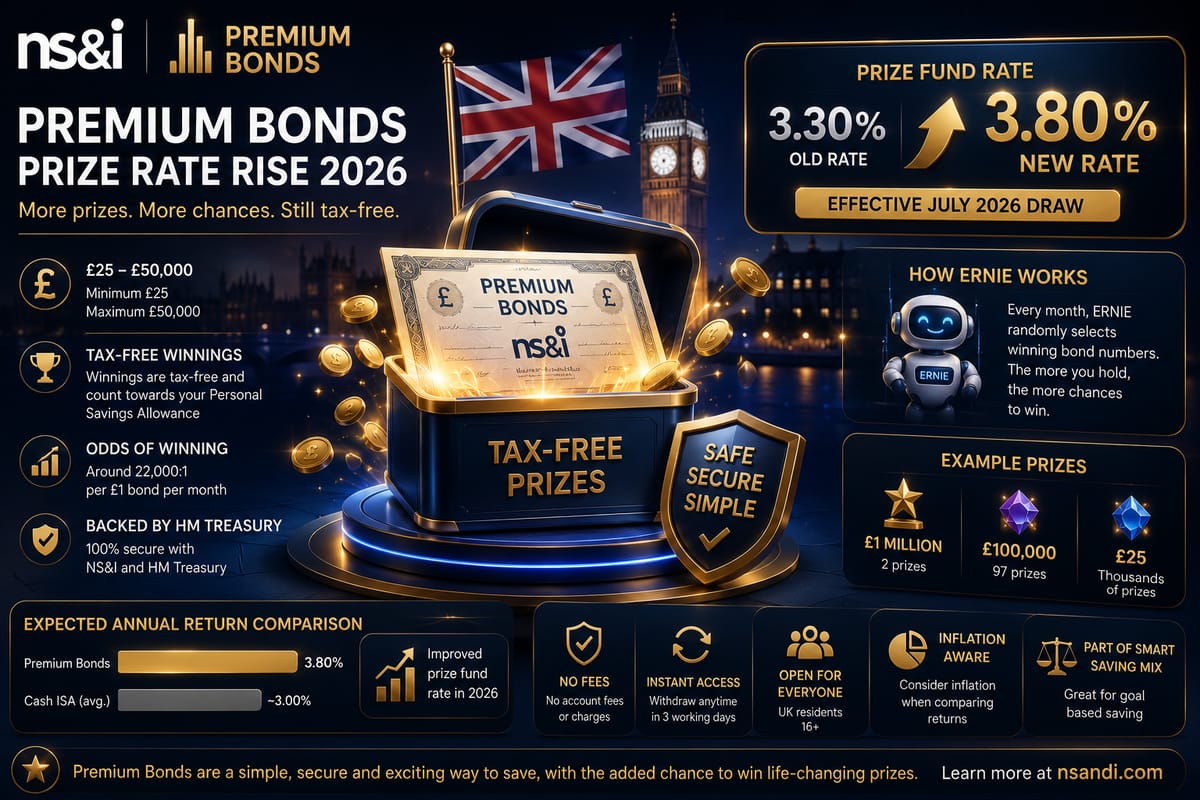

National Savings & Investments (NS&I) has announced a significant increase to the Premium Bonds prize fund rate, raising it from 3.30% to 3.80% effective from the July 2026 draw. This marks the first rate increase in almost three years, following a series of cuts that began in March 2024 from the September 2023 peak of 4.65%. Alongside the rate increase, NS&I has shortened the odds of winning from 23,000-to-1 to 22,000-to-1 per £1 bond, the first odds improvement since the rate was cut in April 2026.

This change delivers an estimated 322,000 additional prizes each month compared to the May 2026 draw, with the total monthly prize fund increasing by over £60 million to approximately £436.8 million. The improved rate also brings NS&I's Direct ISA to 3.80% AER, Direct Saver to 3.45% AER, and Income Bonds to 3.40% gross/3.45% AER, effective from 14 May 2026.

With over 22 million Premium Bonds holders and more than £133 billion invested, Premium Bonds remain the UK's most popular savings product. This comprehensive guide explains everything you need to know about the 2026 rate change, what it means for your returns, how Premium Bonds really work, and whether they are the right choice for your savings in the current interest rate environment.

Quick Summary of the July 2026 Changes

| Metric | Before April 2026 | April 2026 | July 2026 (New) |

|---|---|---|---|

| Prize Fund Rate | 4.00% | 3.30% | 3.80% |

| Odds per £1 Bond | 22,000:1 | 23,000:1 | 22,000:1 |

| Monthly Prize Fund | ~£450M | ~£339M | ~£436.8M |

| Total Monthly Prizes | ~5.9M | ~5.7M | ~6.27M |

| Extra Prizes vs May 2026 | — | — | +322,000 |

How Premium Bonds Actually Work

Premium Bonds are a unique savings product issued by NS&I, an executive agency of HM Treasury. Unlike conventional savings accounts that pay a guaranteed interest rate, Premium Bonds operate on a prize draw model. Every £1 you invest buys one bond with a unique number, and that number is entered into a monthly prize draw conducted by ERNIE (Electronic Random Number Indicator Equipment) — now in its fifth generation using quantum random number generation.

Key Features

- Minimum Investment: £25

- Maximum Holding: £50,000 per person

- Capital Security: 100% backed by HM Treasury — your money is safe regardless of what happens in financial markets

- Liquidity: Withdraw at any time with no penalty (typically 3 working days for online accounts)

- Tax Treatment: All prizes are completely free of UK Income Tax and Capital Gains Tax

- Draw Frequency: Monthly, on the first working day of each month

- Prize Range: £25 to £1 million, with two £1 million jackpots awarded every month

Prize Distribution Breakdown (July 2026)

NS&I allocates the prize fund across three value bands. The distribution is intentionally skewed to create headline jackpot prizes:

| Prize Value | Number of Prizes | Monthly Total | Band Allocation |

|---|---|---|---|

| £1,000,000 | 2 | £2,000,000 | Higher (10%) |

| £100,000 | 83 | £8,300,000 | Higher |

| £50,000 | 167 | £8,350,000 | Higher |

| £25,000 | 334 | £8,350,000 | Higher |

| £10,000 | 835 | £8,350,000 | Higher |

| £5,000 | 1,667 | £8,335,000 | Higher |

| £1,000 | 17,472 | £17,472,000 | Medium (10%) |

| £500 | 52,416 | £26,208,000 | Medium |

| £100 | 1,945,344 | £194,534,400 | Low (80%) |

| £50 | 1,945,344 | £97,267,200 | Low |

| £25 | 2,306,675 | £57,666,875 | Low |

| Total | 6,270,339 | £436,833,475 | 100% |

Understanding the Prize Fund Rate: Mean vs Median

The single most important concept to understand about Premium Bonds is the difference between the mean (average) return and the median (typical) return.

The Mean (Expected) Return

The headline 3.80% prize fund rate is the mean return — it represents the mathematical average across all bondholders. If you divide the total prize fund by the total value of all bonds in issue, you get 3.80%. This is the figure NS&I advertises, and it is what you would earn if returns were distributed equally. However, they are not.

The Median (Typical) Return

The median return is what a bondholder with exactly average luck would actually receive. Because the prize distribution is heavily skewed by the two £1 million monthly jackpots — along with the high-value prizes that make up the top 10% of the prize fund — most individual bondholders earn less than the headline rate. The median return varies significantly based on your holding size:

| Holding Amount | Expected Annual Return (Mean) | Median Annual Return (Typical) | Median Rate |

|---|---|---|---|

| £1,000 | £38 | £0 | 0.0% |

| £5,000 | £190 | ~£95 | ~1.9% |

| £10,000 | £380 | ~£305 | ~3.05% |

| £25,000 | £950 | ~£840 | ~3.36% |

| £50,000 | £1,900 | ~£1,650 | ~3.30% |

Note: Median figures are statistical approximations based on the prize distribution. Actual results vary by luck.

Why Median is Lower Than Mean

The skew comes from the way NS&I structures the prize fund. 10% of the fund goes to high-value prizes (£5,000 to £1 million) that very few people win. The two £1 million jackpots alone account for about 0.5% of the prize fund but benefit only two people per month out of over 22 million holders. This means the 'average' return is pulled upward by a tiny number of large winners, while the vast majority of bondholders receive mostly £25-£100 prizes.

The more bonds you hold and the longer you hold them, the closer your personal return converges toward the headline rate. A £50,000 holder expecting approximately 27 prizes per year has a much more stable and predictable return than a £5,000 holder expecting 2.7 prizes per year.

Premium Bonds vs Cash ISAs: Which is Better in 2026?

The comparison between Premium Bonds and Cash ISAs depends critically on your tax situation and your risk tolerance for variable versus guaranteed returns.

The Tax Perspective

| Taxpayer Type | Personal Savings Allowance (PSA) | ISA Allowance | Tax on Savings Interest |

|---|---|---|---|

| Basic Rate (20%) | £1,000/year | £20,000/year | 0% within PSA, 20% above |

| Higher Rate (40%) | £500/year | £20,000/year | 0% within PSA, 40% above |

| Additional Rate (45%) | £0 | £20,000/year | 45% on all interest |

For basic-rate taxpayers: A top easy-access Cash ISA currently pays around 4.5% guaranteed. On £10,000, that is £450 tax-free guaranteed — versus a median of ~£305 from Premium Bonds. The Cash ISA is clearly superior for this group.

For higher-rate taxpayers who have used their ISA allowance: Once your £20,000 ISA limit is exhausted and your savings interest exceeds £500 (your PSA), any additional interest in a standard savings account is taxed at 40%. A savings account paying 4.5% becomes an effective 2.7% after tax. In this scenario, Premium Bonds become competitive — the median return of ~3.05% on £10,000 is tax-free and may exceed the after-tax return from a savings account.

For additional-rate taxpayers: With no PSA, savings interest is taxed at 45%. A 4.5% account yields just 2.48% after tax. Premium Bonds' tax-free status makes them highly attractive for this bracket.

The Certainty Factor

Even if the median returns are close, there is a fundamental difference: a Cash ISA provides a guaranteed, predictable return that you can budget around. Premium Bonds provide a variable return where you might win nothing for several months then receive several prizes at once. For emergency funds or savings goals with a fixed timeline, the predictability of a Cash ISA is usually preferable.

Historical Context: How Premium Bonds Rates Have Changed

Premium Bonds prize fund rates have fluctuated significantly over the past decade in response to Bank of England base rate changes and market conditions:

| Effective From | Prize Fund Rate | Odds |

|---|---|---|

| July 2026 | 3.80% | 22,000:1 |

| April 2026 | 3.30% | 23,000:1 |

| August 2025 | 3.60% | 22,000:1 |

| April 2025 | 3.80% | 22,000:1 |

| January 2025 | 4.00% | 22,000:1 |

| December 2024 | 4.15% | 22,000:1 |

| March 2024 | 4.40% | 21,000:1 |

| September 2023 | 4.65% | 21,000:1 |

| August 2023 | 4.00% | 22,000:1 |

| July 2023 | 3.70% | 24,000:1 |

| January 2023 | 3.00% | 24,000:1 |

| October 2022 | 2.20% | 24,000:1 |

| December 2020 | 1.00% | 34,500:1 |

The current 3.80% rate is in the middle of the historical range and reflects the current higher-interest-rate environment compared to the 2010s.

Your Odds of Winning: A Detailed Breakdown

Per £1 Bond Per Month

Each £1 bond you hold has a 1 in 22,000 chance of winning any prize in each monthly draw. This means:

| Holding | Monthly Win Chance | Expected Annual Prizes | Chance of Winning Nothing (1 Year) |

|---|---|---|---|

| £1,000 | 4.5% | 0.55 | ~57.8% |

| £5,000 | 22.7% | 2.73 | ~6.5% |

| £10,000 | 45.5% | 5.45 | ~0.4% |

| £25,000 | ~100% | 13.6 | <0.01% |

| £50,000 | ~227% | 27.3 | ~0.0001% |

Note: A monthly win chance above 100% means you statistically expect more than one prize per month on average.

Odds of Winning Specific Prize Amounts

The odds of winning specific prizes vary enormously. With a single £1 bond in a single monthly draw, your chances are:

- £1,000,000 jackpot: 1 in 64.4 billion (effectively zero for practical purposes)

- £100,000: 1 in 1.6 billion

- £25 prize (most likely): 1 in 71,364

With £10,000 invested over one year, your chance of winning at least one £1,000+ prize is approximately 1 in 625, and your chance of winning any prize at all is approximately 99.6%.

Tax Treatment of Premium Bonds

All Premium Bonds prizes are completely tax-free in the UK. This means:

- No Income Tax is payable on any prize, regardless of amount

- No Capital Gains Tax is payable

- Prizes do not count toward your taxable income

- Prizes do not count toward your Personal Savings Allowance

- There is no reporting requirement on your Self Assessment tax return

This tax-free status is particularly valuable for:

- Higher-rate (40%) taxpayers who would otherwise pay 40% on savings interest above their £500 PSA

- Additional-rate (45%) taxpayers who have no PSA and would pay 45% on all interest

- High-net-worth individuals who have already utilised their £20,000 annual ISA allowance

The tax-free nature means that the taxable equivalent rate of Premium Bonds is significantly higher for higher-rate taxpayers. For example, the 3.80% headline rate is equivalent to a taxable savings account paying 6.33% for a higher-rate taxpayer and 6.91% for an additional-rate taxpayer.

How ERNIE Generates Winning Numbers

ERNIE (Electronic Random Number Indicator Equipment) is the system that selects winning Premium Bonds numbers. Now in its fifth generation (ERNIE 5, rolled out in 2019), the system uses quantum random number generation based on the quantum behavior of photons.

Unlike computer-generated pseudo-random numbers (which use mathematical algorithms that are technically predictable), quantum random number generation is truly random. ERNIE 5 detects the random behavior of individual photons passing through a beam splitter — a fundamentally unpredictable quantum process. This ensures that every bond has an exactly equal chance of winning in every draw, with no pattern, bias, or predictability.

The name ERNIE is both an acronym and a tribute: it stands for Electronic Random Number Indicator Equipment and is also a reference to Ernest Marples, the UK Postmaster General who introduced Premium Bonds in 1956.

Optimising Your Premium Bonds Strategy

1. The ISA-First Rule

Before investing in Premium Bonds, ensure you have maximised your £20,000 annual ISA allowance. A Cash ISA paying 4.5% guaranteed almost always beats Premium Bonds for basic-rate and most higher-rate taxpayers.

2. Hold the Maximum for Best Returns

The closer your holding is to the £50,000 maximum, the more predictable your returns become. Small holdings (£1,000-£5,000) are dominated by randomness and may produce no prizes at all for extended periods.

3. Use as a Higher-Rate Tax Shelter

Premium Bonds are most effective as a tax-efficient home for cash savings once your ISA allowance and Personal Savings Allowance are fully utilised. For higher-rate taxpayers with significant cash savings, the tax-free prizes can provide a better after-tax return than standard savings accounts.

4. Consider Family Holdings

Parents can hold Premium Bonds on behalf of their children (under 16), up to £50,000 per child. This effectively increases the total family holding limit and can be a tax-efficient way to save for children's futures, as children have their own Personal Savings Allowance.

5. Reinvest Your Prizes

You can choose to automatically reinvest prizes into additional Premium Bonds. This compounds your holding and increases your future chances of winning, similar to the compounding effect of reinvesting dividends in an investment portfolio.

Conclusion: Are Premium Bonds Worth It in 2026?

The July 2026 rate increase to 3.80% with improved 22,000:1 odds makes Premium Bonds more attractive than they have been in several months. However, they are not the right choice for every saver.

Premium Bonds are best for:

- Higher-rate and additional-rate taxpayers who have exhausted their ISA allowance and Personal Savings Allowance

- Savers who view the 'lottery thrill' as a valuable feature rather than a drawback

- Those who prioritise capital security above all else (100% HM Treasury backed)

- Emergency funds where you want the chance of a return but need immediate access to capital

Premium Bonds are less suitable for:

- Basic-rate taxpayers with unused ISA allowance (Cash ISAs offer higher guaranteed returns)

- Anyone needing predictable regular income from their savings

- Small savers with less than £5,000 who may win nothing for extended periods

- Short-term savings goals with fixed timelines where you need certainty

Before investing, use our Premium Bonds Expected Return Calculator to model your specific holding size and see your realistic median returns, odds of winning nothing, and inflation-adjusted outcomes.